Reporting by Ash Mojica and Geovanni Esparza

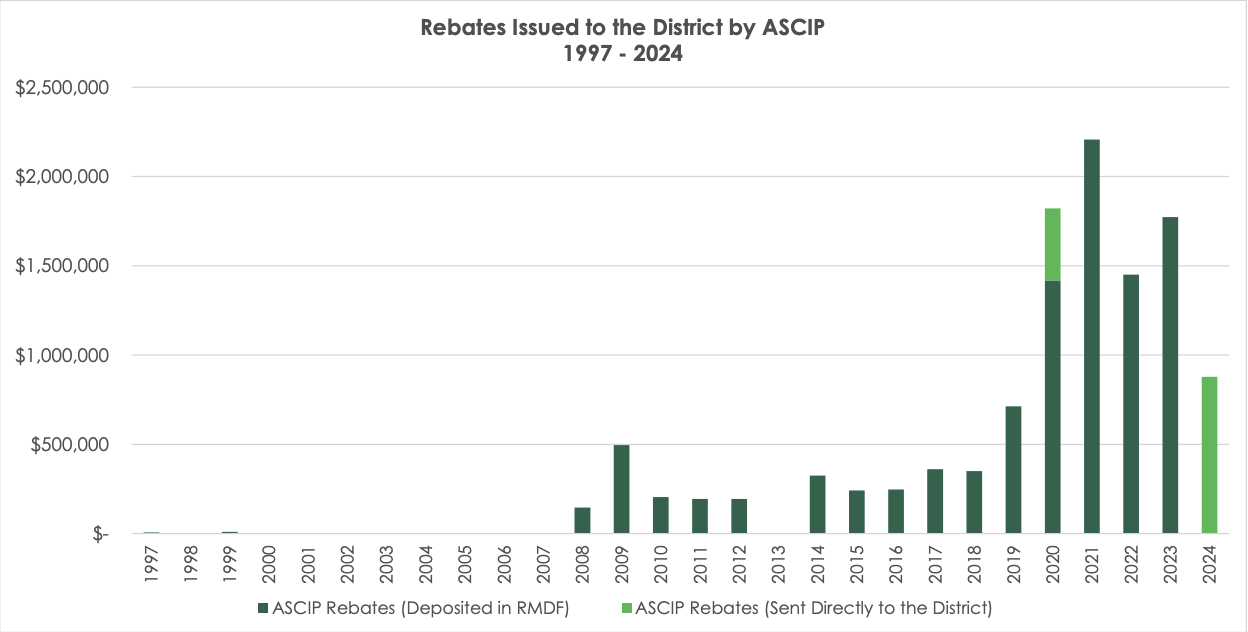

Conflicts of interest between former district administrators. Multiple state and municipal code violations. Undisclosed spending of taxpayer dollars. These findings and more are laid out in a 46-page audit of an off-the-books rebate account held outside the district by a third-party vendor. The audit showed over $12 million was used by the district over more than a decade without disclosing it to the board of trustees or the account appearing on any of the district’s public fiscal reports.

Last fall, the board approved an audit of the nearly 30-year-old account after members discussed its existence and the potential misuse of funds at a board meeting in October. The independent report revealed around a dozen transactions totaling over $12 million from 2010, including withdrawals for a $1 million lawsuit settlement, $1 million to install emergency blue phones at SAC, and nearly $2 million to balance the budget during the COVID-19 pandemic.

Marvin Martinez, Rancho Santiago Community College District Chancellor, stated in the March 25 meeting, “All the funds involved that they were referring to in the report have been accounted for. This fund accounts for less than 1% of our total budget.”

The forensic audit includes the history between RSCCD and the Alliance of Schools for Cooperative Insurance Programs, which includes overlap between district administrators serving as executive members of the nonprofit organization. The report also includes records of the rebate account in emails, memos and further transactions that current district administrators signed off on.

Here are five findings worth learning about and looking into.

#1 The funds in the account were kept from the public and the board

The account, known as a “Risk Management Deposit Fund,” was held by ASCIP for the district as an interest-accruing place to deposit rebates from insurance companies paid out at the end of each fiscal year. Since 1997, it has held taxpayer money that did not appear on any of the district’s fiscal audits, nor was it officially disclosed to the board of trustees.

There were no parameters specifying how the district could use the funds, and the monies held in the account were used to lessen potential risks.

“There isn’t a law that says if you’re keeping a ‘slush fund’, here are the rules. All you can do is best practices,” said Phillip Yarbrough, Trustee and former Fiscal Committee Chair, in a March phone interview.

“Best practices” is a legal term that allows rules from one situation to be applied to another due to uncertainty.

Failing to present receipts of the account’s existence is against the California Code of Regulations, Title 5, Section 58300, which states, “each community college district shall prepare and keep on file for public inspection a statement of all receipts and expenditures of the district.”

According to the audit, the lack of “sufficient information for the Board to govern the District’s use of excess funds” is also against what is required under California Code of Regulations, Title 5, Section 58308.

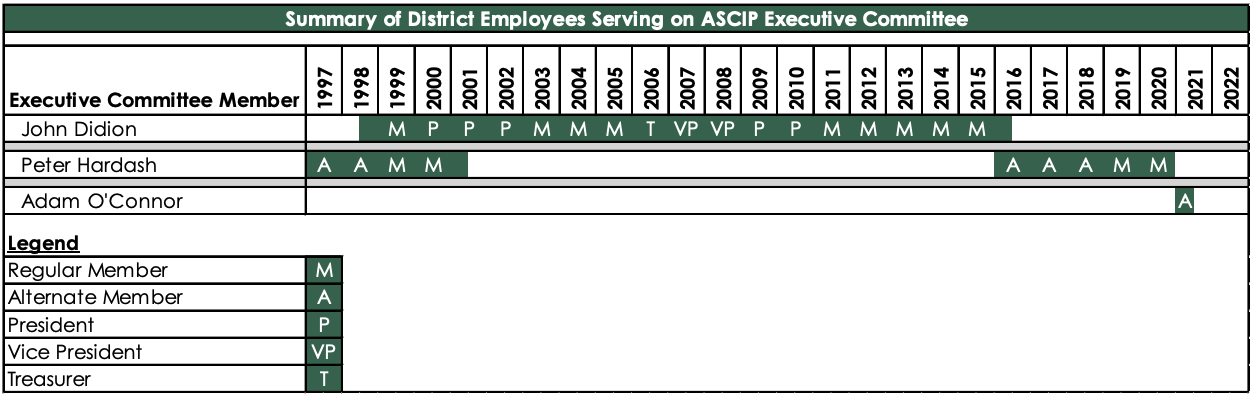

#2 District administrators served as ASCIP’s board members

Two former RSCCD vice chancellors, John Didion (Human Resources and Educational Services) and Peter Hardash (Vice Chancellor of Business Operations/Fiscal Services), were ASCIP board members while they were also in direct control of insurance and fiscal decisions at the district.

Didion served as ASCIP’s president on and off from 2000 to 2010, while Hardash was a member of the executive committee on and off from 1997 to 2020. Didion retired from the district in 2016, and Hardash followed suit in 2019.

During their time as members of the ASCIP board, Didion and Hardash oversaw the district’s decision to send the annual rebates from ASCIP to the fund.

Following the audit, some board members expressed a need for those involved to be held accountable. Other trustees believe it is too late for accountability and that the current board should move on and try not to make the same mistakes.

“Held accountable? The people from 1997? Who are you holding accountable when you think about the practice that’s been routine for the last 20 years, 25 years? Who are you gonna hold accountable?” said Trustee David Crockett. “I think this is a lesson learned in recovery. That’s what I see. Sort of clean up.”

The audit reports that Hardash may have made decisions for ASCIP’s benefit, stating, “Mr. Hardash’s recommendation to defer the rebate from ASCIP appeared to be based on the best interest of ASCIP, and not necessarily the District.”

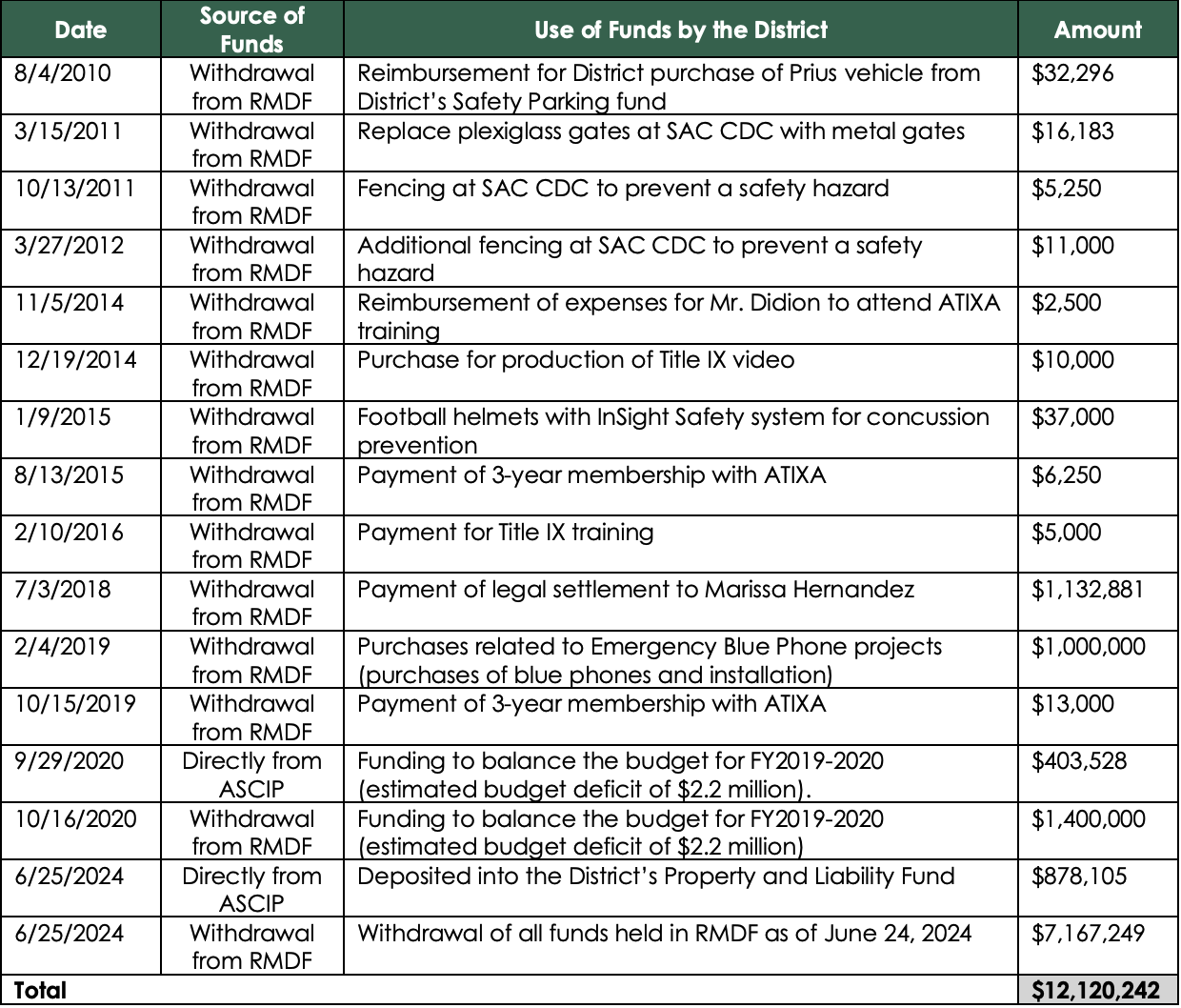

#3 Former officials used the funds for over a dozen miscellaneous purchases since 2010

The audit provided a list of purchases using money from the RMDF going back to 2010. The funding source of these transactions was never disclosed to the board or the public. Hardash approved multiple transactions ranging from $2,500 to over $1 million.

In 2010, the district used the fund to reimburse $32,296 spent on a Prius with the District Safety Parking fund.

One of the biggest withdrawals from the account was the payment of a legal settlement of $1.1 million for a wrongful termination lawsuit from 2018.

Marvin Martinez said in an interview, “There was no evidence that’s ever been found that there was a secret scheme and plan to keep the board away from that. Because if there were a scheme, then you would maybe have found that there was misuse of funds, that the funds were misappropriated, and the funds were used to do things that you should not be using them [for].

Smaller purchases included payment for fencing, football helmets and emergency blue phones.

District officials justified these purchases as they were all used to address risks.

“The purpose of the blue phones is so that in case there’s anything that anyone sees, or if you’re being stalked or followed, or you see something, you can use the phone to call, and that minimizes risk,” said Chancellor Martinez.

According to the audit, “Prior to 2020, funds withdrawn from the RMDF by the District were deposited into District accounts to be used by the District for specific one-time purchases.”

The biggest purchase was made in the fall of 2020 when the district withdrew nearly $2 million from the RMDF.

#4 Current administrators used the fund to balance the budget

In 2020, district officials used $1.4 million from the RMDF to balance Santa Ana College’s budget. Community college enrollment across the state declined in the years leading up to the pandemic. During spring 2020, however, SAC saw a steep and immediate decline in enrollment and was on track to present an unbalanced budget. It was one of the last withdrawals to be made from the RMDF.

“You’re not allowed to present an unbalanced budget, so the funds were used to help balance that budget. So one of the things that the [auditor] said is that, because at that time, there were no parameters provided on how the monies were to be used, you can use it for almost anything,” said Martinez.

In 2020 and 2024, funds from the RMDF were deposited into district accounts without a designated purpose.

The most recent transactions put the withdrawn funds into the district’s general fund.

#5 The fund’s existence may violate more than a few codes

Multiple other code violations were reported within the audit and called out by board members at meetings last month.

The audit concluded that the ASCIP rebates held in the RMDF were not reported in the district’s financial statements and were not in accordance with RSCCD’s Budget Allocation Model, which dictates that rebates should be deposited into the institutional reserves.

The district’s administrative regulations were also violated because they were not disclosed to the public or included in the district’s financial audit statements.

The district’s administrative regulations state that when district officials manage district investments, they should avoid any transactions that might impair public confidence.

“I’m very upset about the deceit that’s been going on about keeping this from our auditors and keeping this from our board,” said Yarbrough. “A fund of almost $8 million kept secret from us, from everybody, in violation of the law.”

Chancellor Martinez has hired a legal team to look into the violations.

“You need to ask the experts. The accountants were trying to do their best, but they’re not attorneys. Let’s have some real attorneys [look at it],” said Martinez. “As soon as I have that analysis, we’ll first show it to the board, then we’ll put it out there in public so everyone can see.”

Read and download the full audit below:

- In Photos: Washington D.C. during the government shutdown - October 23, 2025

- Attend public meetings to remind elected officials they serve you - October 13, 2025

- District approves funds to move broadcasting studio to main campus - September 23, 2025

The concept of “Best Practices” is not a legal term that directly allows applying rules from one situation to another due to uncertainty. While “Best Practices” is often used to guide actions and decisions, it’s not a formal legal concept.

“Best practices” generally refer to recommended approaches or methods considered effective and efficient in a particular context, but they are not legally binding or enforceable.

“Best practices” are often associated with softer forms of guidance, while legal rules are considered “hard law” and are more strictly enforced.

While “Best Practices” are helpful guidelines, they don’t function as legal rules. They are not meant to be applied universally or to override specific legal obligations.